Which private sector industries "pay the bills" for British Columbia?

Productivity isn’t everything, but in the long run it is almost everything.

A country’s ability to improve its standard of living over time depends almost entirely on its ability to raise output per worker.

~ Nobel Laureate Paul Krugman, 1997

A society’s standard of living ultimately depends on its labour productivity, that is, its ability to generate the highest possible level of income per unit of labour.[1]High labour productivity results from the intensive use of physical and intangible organizational capital to produce goods and services, along with advanced skills and technologies, economies of scale, and agility in shifting inputs across firms and industries to their highest value use.

British Columbia has historically had a high standard of living relative to many other jurisdictions. Which industries are central to that result? Which sectors generate high levels of income and tax revenues to fund public services? And after COVID-19 ends, which industries are critical to the recovery of pre-pandemic income levels?

What are B.C.’s highest value-added sectors?

B.C.’s highest value-added sector – by far – is natural resource production (Figure 1). The mining, oil and gas production sector generates five times as much value-added (real GDP at basic prices) per unit of labour input as the business sector overall ($53 per hour).[2]The sector’s openness to international competition and trade engenders its intensive use of capital, skills, advanced technologies, and economies of scale.

For every hour worked in the natural resource sector in 2018, B.C. reaped $248 of real GDP. The next highest GDP per hour sectors are utilities ($203), leasing ($151), information and cultural industries ($85), and finance and insurance ($80). The high levels of income (and export earnings) generated upstream from B.C.’s highest GDP per hour sectors directly and indirectly create demand downstream for other sectors of the economy (e.g. transport services, wholesale trade services and professional services, as well as consumer-facing sectors).

Figure 1

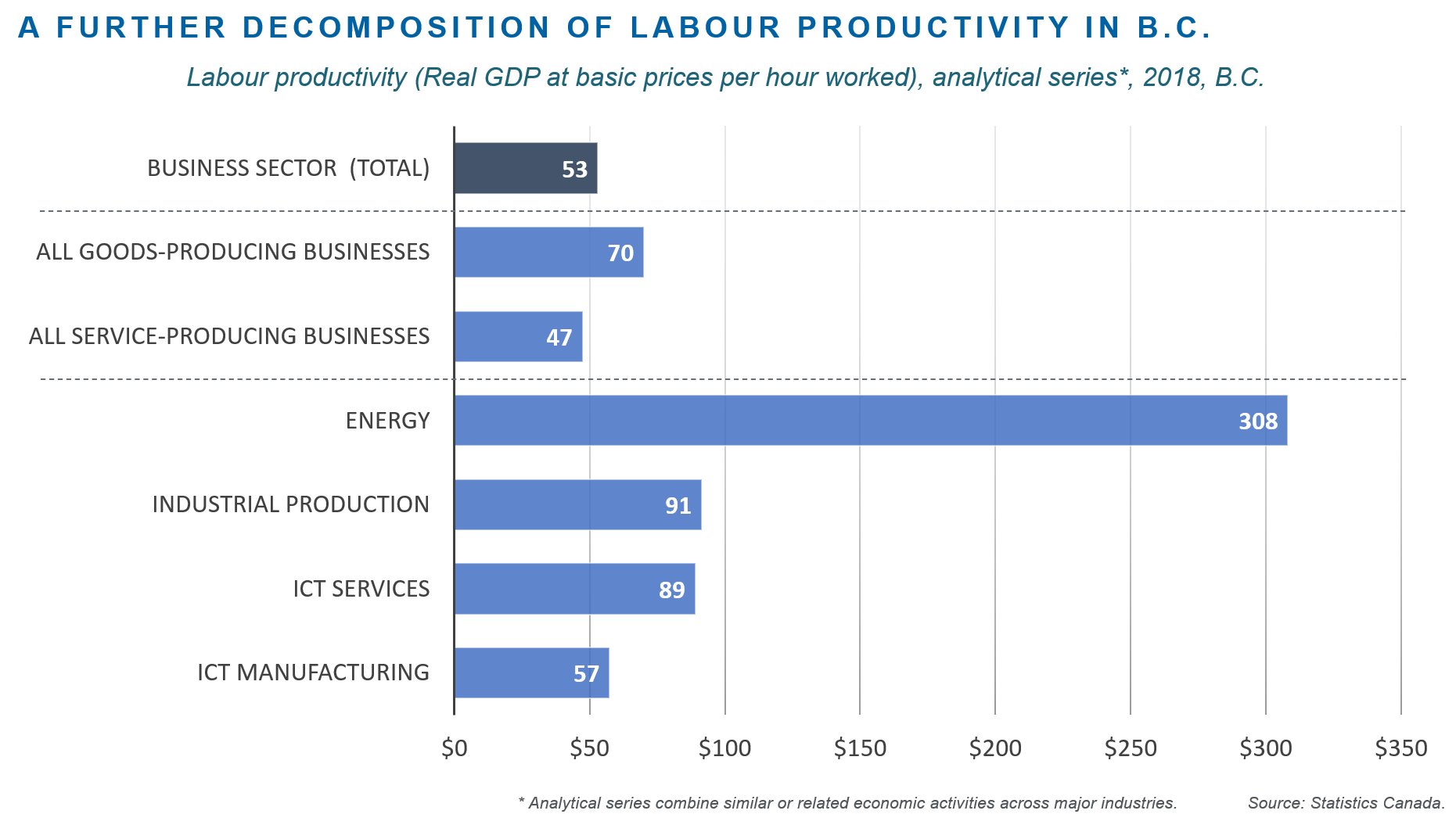

Figure 2 examines labour productivity by type of economic activity.[3]On average, goods-producing industries generate $70 in real GDP per hour of employment, while services-producing industries generate $47 per hour. The chart also shows some analytical series that group similar economic activities across several industries. Activities related to energy production and distribution generate – by a wide margin – the highest real GDP per hour of employment ($308). This is about six times the average for the business sector overall ($53). Other high productivity activities involve industrial production ($91), production of information and communications (ICT) services ($89) and, to a lesser extent, ICT manufacturing ($57).

Figure 2

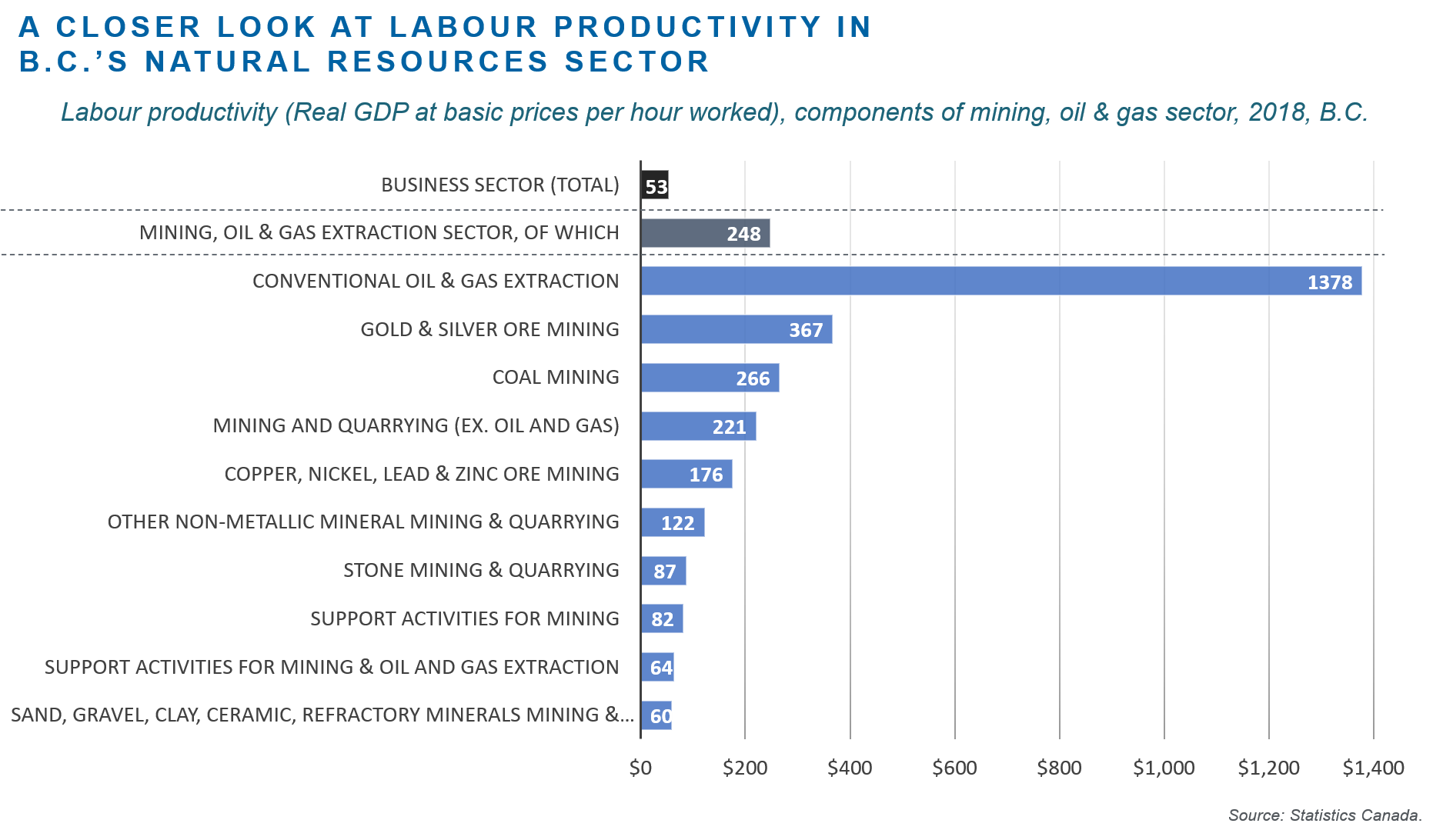

Lastly, Figure 3 looks at the natural resources sector in more detail. It highlights the outsized contribution of B.C.’s conventional oil and gas sub-sector – most of which relates to natural gas – to provincial GDP. In 2018, the oil and gas sub-sector yielded $1,378 in real GDP per hour of employment. That is a whopping 26 times the average GDP per hour of the business sector overall ($53). Gold and silver ore mining ($367 per hour), coal mining ($266) and other types of mining, quarrying and other natural resource activities also generate very high levels of GDP per hour.

Figure 3

Conclusion

The COVID-19 pandemic has punched a deep hole in B.C.’s economy. Hundreds of thousands of workers have lost their jobs and are unsure when or if they will be reemployed. Record numbers of businesses could be headed for permanent closure or bankruptcy. Business capital spending has collapsed, as have the tax revenues needed to pay for public services without taking on more public debt. To prevent entrenched hardship, the hole in GDP needs filling, quickly.

The quickest, surest path for B.C.’s post-pandemic recovery is to fire up the province’s big economic engines. This need not involve a heavy fiscal cost, but rather reviewing and adjusting B.C.’s tax and regulatory settings to ensure they are not too inefficient, antiquated and discouraging of private-sector investment and hiring – particularly in our leading industry sectors. In simple terms, these sectors “pay the bills” for B.C. They generate high levels of real GDP per hour, catalyze demand across other sectors and, directly and indirectly, contribute the tax revenues B.C. relies on to sustain its public services. Absent the horsepower from its major economic engines, B.C. will likely struggle to quickly recover pre-pandemic income levels.

[1] Small open economies also benefit from favourable movements in their terms of trade (i.e. when export prices rise faster than import prices). However, export and import prices are generally determined by international market forces rather than domestic policy settings.

[2] The “business sector (total)” combines the business establishments in the North American Industry Classification System (NAICS) codes 11-81, with the exception of the owner-occupied dwellings industry.

[3] For the analytical series shown in Figure 2: “goods-producing industries” combines the business establishments in the NAICS codes 11, 21, 22, 23, 31-33; “services-producing industries” combines codes 41, 44-45, 48-49, 51, 52, 53, 54, 55, 56, 61, 62, 71, 72, and 81 with the exception of the owner occupied dwelling industry; “energy” combines codes 211, 2121, 212291, 21311A, 2211, 2212, 32411, 486; “industrial production” combines codes 21, 22, 31-33 and 562; “ICT services” combines codes 4173, 5112, 517, 518, 5415 and 8112; and “ICT manufacturing” combines code 334 excluding 3345.