B.C. fiscal plan gets a thumbs down from S&P Global ratings agency

British Columbia has regressed to an era of sizable government operating deficits and fast-growing debt, even with an inflationary and overheated economy. That is the main takeaway from the 2023 provincial budget tabled in late February. After several years of operating surpluses (punctuated by a temporary deficit during the COVID-19 recession) - and despite the economy being beyond full employment - B.C. is planning for a steady flow of red ink over the next three years (at least). Budget 2023 pencils in a $4.2 billion operating deficit this year, followed by deficits of $3.6 and $3.1 billion in the next two years. In addition, the NDP government is ramping up capital spending – which does not show up directly in the operating budget – resulting in further increases in net public sector debt.

B.C.’s net debt will jump sharply both in absolute terms and as a share of GDP. Net debt is projected to reach 23% of GDP by mid-decade, almost ten percentage points higher than in 2018-19. With incremental borrowing more expensive in a higher interest rate environment, and government required to roll over a portion of its existing debt every year, the province is looking at steadily escalating debt-servicing costs over the rest of the decade.

S&P Global downgrades B.C. government’s credit rating

All of this has caught the attention of the credit-rating agencies. S&P Global has downgraded the province’s credit rating to ‘AA’, from ‘AA+’, which will make debt issuance slightly more expensive for the province and its Crown corporations (see S&P’s press release here).

In justifying the downgrade, S&P observed:

“The Province of British Columbia's (B.C.) 2023 budget outlines an extensive investment plan for operations and record levels of capital spending, which will reverse the fiscal gains made in the past two years and result in the return of operating deficits, larger after-capital deficits, and a relatively steep increase in debt through to fiscal 2026.

On April 18, 2023, S&P Global Ratings lowered its ratings, including its long-term issuer credit rating, on the province, as well as its issue-level rating on British Columbia Hydro & Power Authority's (BC Hydro) provincially guaranteed senior unsecured debt, to 'AA' from 'AA+'. The outlook is negative. S&P Global Ratings also affirmed its 'A-1+' short-term rating on B.C.”

In explaining their negative ratings outlook, S&P said:

“The negative outlook reflects a one-in-three chance that we could lower the ratings in the next two years if, in our view, the province's commitment to fiscal consolidation continues to waver as reflected by large after-capital deficits, increasing debt, and very low levels of internal liquidity.

We could lower the ratings in the next two years if B.C. sustains after-capital deficits greater than 10% of total revenues, reflecting the province's limited use of fiscal flexibility.

A reversal of the current fiscal trajectory as evidenced by a return to operating surpluses and modest after-capital deficits of about 5% of total revenue, a slowing growth trend in the province's tax-supported debt burden, and improving liquidity metrics of more than 40% of next 12 months' debt service in the next two years, could lead us to revise our outlook to stable.”

With respect to the economic outlook, S&P observed:

“We expect that, following a strong year, B.C.'s economic prospects will wane in 2023, largely due to elevated levels of inflation and high interest rate.

[W]we forecast that B.C.'s GDP per capita will remain in line with the national figure of about US$54,900 for 2023. The province has considerable economic strengths, such as its position on the west coast of Canada and its proximity to Asian markets, as well as large natural resource assets. We expect the economy will remain well diversified. Key sectors include forestry, mining and natural gas, financial and real estate services, and construction and manufacturing. In addition, B.C. has a large public sector consisting of government, universities, public schools, and hospitals.

With the release of the current budget, we believe that the province’s commitment to fiscal discipline and stability has waned [emphasis added]. B.C. redeployed a large portion of its better-than-expected year-end surplus to new commitments. In addition, the province is materially increasing its spending for both operations and capital investment to record levels, while economic growth is slowing.”

Opening the spending taps

Since taking office in November 2022, Premier David Eby has opened the spending taps to solve B.C.’s most pressing problems – unaffordable housing, widespread public disorder, and a creaking health care system. Billions of additional taxpayer dollars have been allocated to these high-profile policy areas.

Government spending has been on a tear since 2019 and is projected to reach $82 billion by 2025-26. In 2019-20, B.C. government outlays stood at $58.7 billion, meaning spending will have jumped by 40% in little over half a decade. This is partly explained by higher-than-anticipated inflation during 2021-23, which is now pushing up public sector compensation costs. But it also reflects a political choice to expand the size and reach of government.

Elevated capital spending is a core element in the NDP government’s fiscal plan. Public sector capital investment is estimated at $48.5 billion over the next three years, with about 80% of that being taxpayer-supported; the remainder is capital spending by what are classified as financially self-supporting Crown corporations.

We see economic and social benefits from improving the public sector capital stock. However, the timing is questionable. Dialing up government-mandated investment carries financial and economic risk because it coincides with: (a) an economy operating beyond full employment and overheated by massive fiscal stimulus in Canada, the United States and other advanced countries during the past few years, as highlighted in new research from the St Louis Federal Reserve; (b) inflation that is consequently running above the Bank of Canada’s target; and (c) also as a result, the construction and project development sector is operating near or beyond full capacity.

Several public sector construction projects have already faced significant cost overruns, in part because of the NDP’s “community benefits agreement” (CBA) regime. The CBA creates a set of contracting and procurement rules that favour certain unionised construction firms, thus reducing competition and driving up costs. We expect this pattern of project cost overruns to continue as the B.C. government increases total capital spending by more than 60% between 2021-22 and 2025-26.

What does this mean for living standards in British Columbia?

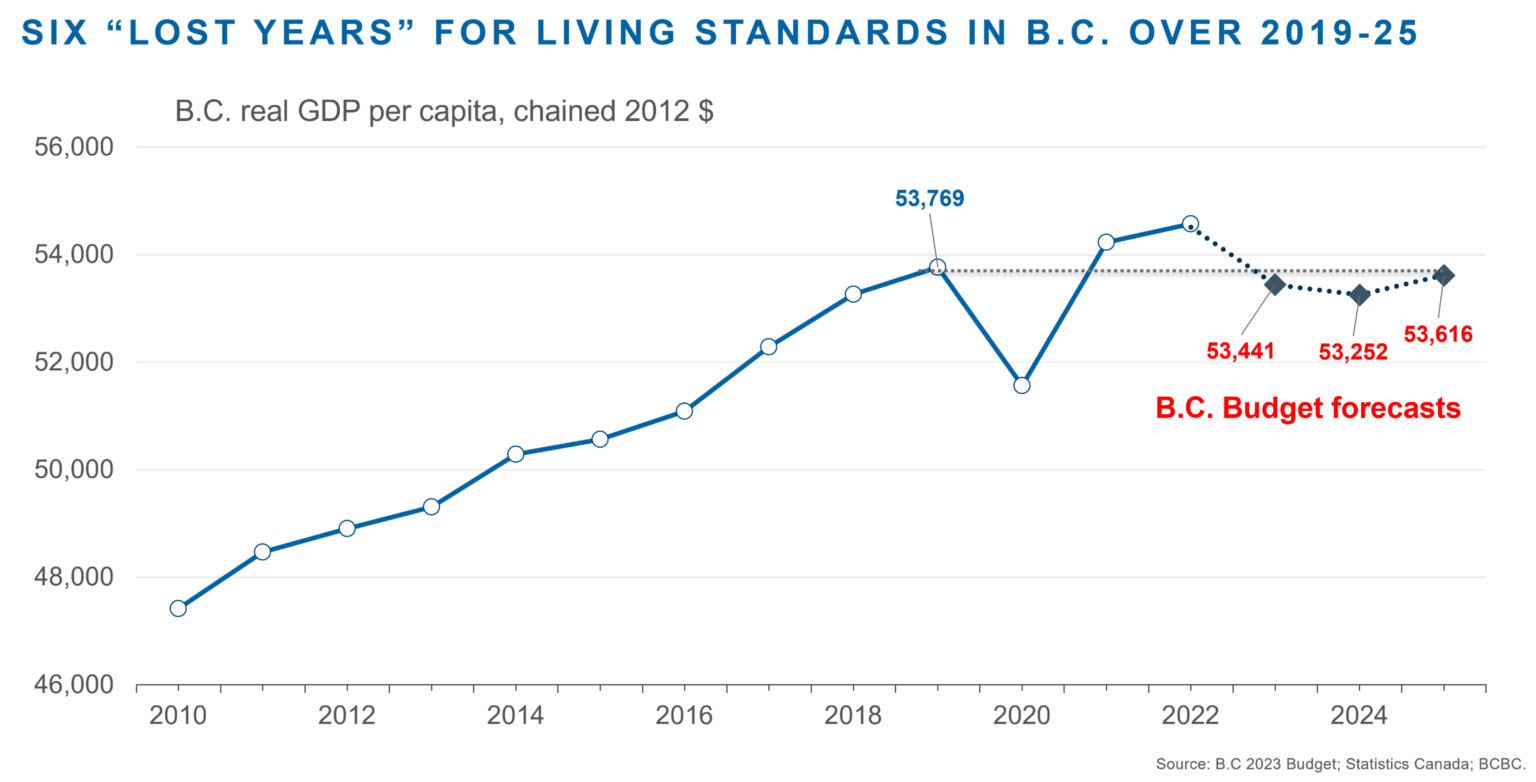

As noted in the Business Council’s reaction to Budget 2023, the government’s decision to expand the public sector is not matched by a commitment to strengthen the private sector. The budget offers little that will improve the business environment and lead B.C.-based companies to step up capital investment here, or encourage entrepreneurial value-creation, or improve lackluster productivity growth. British Columbians are facing (at least) six years of no advancement in average living standards as growth in real GDP per capita stagnates over 2019-2025 (Figure 1).

We conclude with some reassurance that in comparative terms, B.C. remains in decent shape by Canadian standards. While B.C.’s government debt burden is growing rapidly, the net debt/GDP ratio is still below the average of other provinces. S&P points to B.C.’s diversified economy as a reason for optimism about the medium-term fiscal picture. Nonetheless, it is troubling that the government is sharply raising spending and borrowing against a backdrop of stagnating GDP per capita growth over the forecast horizon. And global ratings agencies are taking notice.