Please don’t feed the inflation dragon

As noted in a previous blog, a generation of Canadians has come to expect low, stable growth in consumer prices. The “inflation dragon” of the 1970s and 1980s was considered slain, or at least sound asleep. It has been decades since Canadians have had to wonder about the inflationary side-effects of fiscal or monetary policy (both globally and in Canada).

Today, however, a heady cocktail of extraordinarily loose policy across countries stimulating interest-sensitive segments of demand (especially housing investment and durable goods consumption), combined with supply-side disruptions caused by the COVID-19 pandemic, has acted like a potion of smelling salts to awaken the inflation beast.

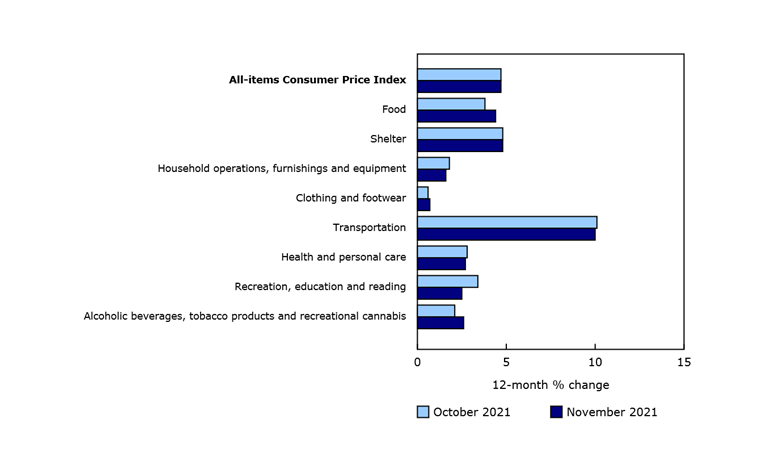

Canada’s inflation rate is almost 5% y/y

Statistics Canada figures show Canada’s consumer price index (CPI) inflation rate at 4.7% year-on-year (y/y) in November – the highest rate of inflation since 1991. All eight major components recorded higher prices, with the largest increases in the transportation and shelter categories (Figure 1). Top contributors to the November result were prices for petrol (+43.6% y/y), furniture (+8.7%) and food (+4.4%). The latter was the largest price hike since January 2015. Excluding petrol, the CPI rose 3.6% year over year, the same as in October. For British Columbia, CPI inflation was 3.6% y/y in November.

By comparison, United Kingdom CPI inflation was 4.6% y/y in November (i.e. similar to Canada’s rate), while American CPI inflation was much higher at 6.8% y/y in November.

Figure 1: Canada faces broad-based CPI pressures

Consumer price index (CPI) by major category, year-on-year change, Canada

Source: Statistics Canada

The post-pandemic recovery in CPI is more than complete

Figure 2 shows the actual level of the all-items CPI from January 2018 compared to the level of CPI had inflation trended at the Bank of Canada’s 2% per annum inflation target over that period. Also shown is the CPI excluding volatile items like food and energy. The COVID-19 pandemic caused a significant but temporary drop in the level of the CPI. However, by August 2021, the level of CPI had fully recovered and caught up to the level implied by the Bank’s target.

As of November 2021, the level of the CPI is well above the level implied by the 2% per annum target since 2018. In other words, CPI growth has more than made up for its weakness during the earlier phase of the pandemic. Moreover, even excluding food and energy prices, the CPI has recovered to the level implied by the 2% per annum target. The raises questions about whether ultra-loose monetary and fiscal policy remains appropriate for the state of the Canadian economy.

Figure 2: CPI level since 2018

CPI level since 2010

Figure 3 shows a decade-long perspective on the level of CPI. It shows the actual level of CPI from January 2010 compared to the level implied by the Bank of Canada’s 2% per annum target. Once again, the chart also shows the CPI level excluding food and energy.

Annual CPI has consistently undershot the Bank’s inflation target since from 2013, resulting in the levelof actual CPI lagging behind that implied by the 2% per annum inflation target. Letting the economy “run hot” during 2021, intentionally or unintentionally, has returned the level of actual CPI to about where it would have been had the 2% per annum target for inflation been met over roughly the past decade.

Figure 3: Unfinished business? CPI has undershot the Bank of Canada’s target since 2013

Canada’s GDP recovery is incomplete

Another motivation for loose monetary and fiscal policy is that Canada’s GDP recovery is incomplete. Figure 4 shows the actual level of GDP compared to the trend in GDP based on the 2010-2019 average growth rate. Despite strong recent growth in GDP, the level of GDP remains below where it would have been absent the pandemic. Again, the question is whether demand-side stimulus has largely run its course and is now contributing to excessive inflation pressures.

Figure 4

Conclusion

As the COVID-19 pandemic persists, Canada’s economy is still in need of some degree of monetary and fiscal support. However, it is hard to argue that it is still in need of emergencylevels of demand-side stimulus. Loose monetary and fiscal policies have successfully boosted demand for housing investment and durable goods consumption but have done little for the rest of the economy – especially business investment and goods exports.

Many advanced economy central banks have recently recanted their view that inflation pressures are “transitory”. This is a good signal. For its part, the Bank of Canada has wound down its quantitative easing through the purchase of new issues of Government of Canada bonds. However, for now, it is maintaining the massive current size of its federal bond holdings rather than letting the portfolio shrink as the bonds mature.

Also, it has issued new forward guidance that it will not raise its policy interest rate from 0.25% until Q2-Q3 2022. Previously, the Bank’s forward guidance was that it would not raise short term interest rates until the second half of 2022.

On fiscal policy, Canada was to our knowledge the only country in the world not to produce a national budget in 2020. Instead, the federal government’s tax and spending plans for 2020/21 were rubber stamped by Parliament with little oversight or scrutiny. The number of parliamentary sitting days in 2020 and 2021 has also been curtailed and are at post-war lows. This week, the federal government belatedly released its fiscal accounts and an update showing its budget deficit for 2020/21 was an eye-watering -$327.7 billion. For 2021/22, the federal deficit is forecasted to be a still very large -$144.5 billion. While these deficits are lower than forecast, that is mainly due to the windfall of higher inflation boosting tax revenues rather than any deliberate action taken by the government.

The OECD projects that Canada will be the worst performing advanced economy in real per capita GDP growth over both 2020-2030 and 2030-2060 (see our previous blog). With ultra-loose monetary and fiscal policy past the point where they are “doing more good than harm”, it is time for Ottawa to look at ways to assist the recovery in GDP through non-inflationary policy adjustments. Structural reforms could include working with the provinces to lower Canada’s byzantine barriers to internal trade (as proposed here), fostering higher business investment per worker (as reviewed here), and reviewing policies that affect the incentives and disincentives facing companies aspiring to operate at scale.